They never saw it coming

Choose your poison: austerity, inflation or default

https://www.pricevaluepartners.com/they-never-saw-it-coming/

“Change is inevitable. Growth is optional.”

John C. Maxwell.

Thousands of people were killed – we will never know quite how many. A cloud of toxic material rose over 20 miles into the sky. The heat energy involved was 100,000 times as intense as that from the atomic bomb that levelled Hiroshima.

When Mount Vesuvius erupted on 24 August, 79 AD, the people of Pompeii and Herculaneum never saw it coming. They had been conscious of earth tremors in the preceding weeks, but didn’t link them to the mountain that overshadowed their towns. There is no Latin word for volcano. The closest is a neologism: mons ignifer (fire-bearing mountain).

Our only source for the disaster is a couple of letters written by Pliny the Younger, who was then a 17-year-old, watching, transfixed, as a huge cloud rose above the mountain:

“I cannot give you a more exact description of its appearance than by comparing it to a pine tree; for it shot up to a great height in the form of a tall trunk, which spread out at the top as though into branches.. Occasionally it was brighter, occasionally darker and spotted, as it was either more or less filled with earth and cinders.”

Then an explosion. More explosions. And suddenly, molten rock and pumice started tumbling from the sky, at a rate of over a million tons a second.

For those not fortunate enough to escape the towns immediately, death would come either by asphyxiation, or incineration, as pyroclastic flows streamed down from the mountain, burning everything in their path.

Three million people live in the close vicinity of Mount Vesuvius today. This part of south-western Italy is the most densely populated active volcanic region in the world.

The next crisis ?

Our primary concern as investors today is not the capricious and chaotic policy-making of President Trump, and not even the self-destructive economic policy-making of so many western administrations for which they have no legitimate democratic mandate. Not directly, at any rate. That word ‘rate’ has a sobering relevance. It has more to do with a situation that has been slowly bubbling away and building a head of steam for years in the world’s largest asset class: bonds.

Much financial commentary post-Brexit (for example) has been pure nonsense. Brexit has been blamed for all kinds of trends in stock and bond markets globally but there can be no counter-factual: we will never know for sure the extent to which markets reacted to the UK vote or did what they were going to do anyway, irrespective of the vote. To the financial media, correlation and causality are the same thing.

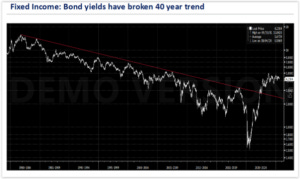

But one thing is clear. Interest rates throughout the world have been in a downtrend that began roughly 40 years ago. That downtrend broke conclusively to the upside about three years ago.

Source: Bloomberg LLP.

As any technical analyst will tell you, once a long term trend breaks, meaningful things happen, and they don’t tend to be positive for those still clinging to the now expired trend. The strategist and market historian Russell Napier makes the following observation:

“You shouldn’t own any fixed interest securities. [Bonds.] None. Inflating away debt means destroying the purchasing power of fixed interest securities. There may be rallies, but fixed income is [now] in a long bear market. Bond bull and bear markets move in about 40 year periods, and we are now into year 3 of the current bear market. You can lose a fortune in real terms over the long term. Therefore: No bonds. Period.”

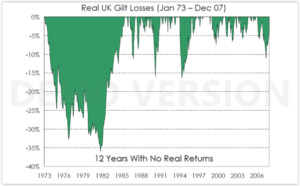

An example from history. The chart below, courtesy of Frontier Capital Management, shows you how UK bond investors were savaged by the grim stagflation of the 1970s. 12 years with no real returns is not a pleasant outcome. And we would argue that our present economic and debt predicament is easily comparable – if not worse – versus the 1970s experience.

Most financial journalists and for that matter analysts tend to cling lazily to asset class stereotypes: bonds are “safe”; equities are “risky”; commodities are “very risky”. But safety in an investment is not an absolute, just as value in an investment is not an absolute. Safety is contextual, and it is dependent not least on price.

The ‘safest’ investment in the world suddenly becomes unsafe if you buy it at an unsustainable price.

And that is precisely where much of the bond market sits today. A benign 40 year downtrend in yields has now reversed. Despite an official national debt of over $38 trillion, President Trump has just stated that he would like to raise the US military budget by over 50% to $1.5 trillion by 2027. The swashbuckling days of DOGE seem a long way away.

The only money that works

Discovering Mises completely transformed our understanding of economics. To Mises and the Austrian School, the only form of money that has any value is sound money. In the words of Eamonn Butler, summarising Mises,

“Money is an economic good, but its purpose is neither production nor consumption. Its purpose is exchange. By printing money governments can create an artificial boom, but this must inevitably be followed by a bust. A painful adjustment process takes place as malinvestments are liquidated. A stable monetary system would have to be based on a commodity standard such as gold.”

We are not saying that we necessarily expect a return to any form of gold standard any time soon. Our point is, rather, that the current monetary system is already living on borrowed time. The financial markets didn’t get an opportunity to purge the system of malinvestments after Lehman Brothers failed. Instead, the central banks of the world circled the wagons and poured trillions of dollars, pounds, euros and yen into the black hole of the credit system to keep bad banks afloat. But the day of reckoning has only been deferred – it has not been cancelled. The market will find a way.

That way already seems to be via gold, which in US dollar terms has risen by 150% over the last five years. Its monetary rival silver has performed even more impressively, rising by 270% in dollar terms over the same period.

Bear in mind that in their seminal account of debt disasters through history, ‘This Time is Different’, Reinhart and Rogoff showed that once any government incurs a debt to GDP ratio much above 90%, bad things happen. In the words of ‘The Economist’:

“[Reinhart and Rogoff] found that public debt has little effect on growth rates until debt reaches 90% of GDP. Growth rates then drop sharply. Over the entire two-century sample (from 1790 to 2009), average growth sinks from more than 3% a year to just 1.7% once debt rises above the critical level..

“The sharpness of this turning-point excited lots of attention. In economic jargon the debt-growth relationship was not “linear”, with growth rates gliding steadily downward as borrowing rises. Instead, debt levels look benign until a critical point is reached, and then they don’t. The authors reckoned that beyond the 90% threshold, market perceptions of risk can jump. That could translate into soaring interest rates or financial-market stress, forcing hard choices: austerity, inflation or default.”

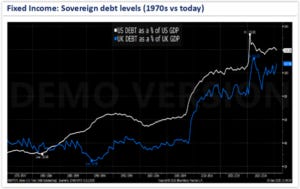

Compare debt to GDP levels in the anglosphere today, versus the 1970s (when the UK’s Labour government was forced to go cap in hand to the IMF for an emergency loan):

Source: Bloomberg LLP.

Austerity, inflation or default.

We’ve flirted with austerity – briefly – and it proved to be too politically unpalatable.

That leaves inflation or default. Neither of which is particularly appealing either. But they may be unavoidable.

Since widespread defaults in government debt would make the global pensions system immediately bankrupt (because pension funds are the single largest holders of government bonds), we have to presume that inflation will be governments’ preferred outcome – which is why, despite its palpable failure to trigger economic growth, even more QE looks certain. Central banks, hedge funds and commercial traders may continue to buy government bonds, whatever the price.

They may wish to. Pension funds have to, courtesy of regulatory pressure. You don’t have to.

To us, the bond market outlook is bad and will get worse. Bonds are still caught in a once-in-a-thousand-year bubble, and when it bursts it will be ugly. The trouble is that nobody knows when this bubble will go bang. The correction has arguably already started.

In which case, the prudent strategy is surely to remove oneself from the vicinity. Give the volcano a wide berth. Be very careful which bonds you own and, if in any doubt, don’t hold any. There is certainly no safety whatsoever in owning the government debt of an insolvent government.

The investment managers Incrementum recently came to the following conclusions:

Growing economic and political uncertainty is boosting and will continue to boost the gold price;

In the light of ongoing geopolitical uncertainty, expect even more monetary stimulus from the ECB to counter the risk of the disintegration of the EU;

The US economy is softening and the normalisation of US interest rates is no longer on the cards;

If the dollar weakens further and commodity prices continue to rise, there is a rising risk of inflation and stagflation (Back to the 70s !);

Instititutional investors are likely to (continue to) rediscover the portfolio benefits of gold;

The inflationary outlook is beneficial to gold but also potentially positive for silver and for precious metals mining stocks;

Gold is back – a new bull market is already happening.

Gold is only an answer, of course, but it’s an important one. As reflected in our own portfolios, given the uncertainties we all face, it makes sense to diversify – value stocks, absolute return funds and cash still have a role to play.

Apocalypse when ?

The bond market explosion could happen quickly – or the debt volcano could keep gently smouldering for years.

But just because something hasn’t happened yet doesn’t mean something can’t ever happen. Just because the bond market hasn’t exploded yet doesn’t mean that it never can or never will. The citizens of Pompeii and Herculaneum must have thought they were perfectly safe, making a living from the verdant slopes of Mount Vesuvius – until it erupted without warning. The point is to be aware of the risks and prepare for them accordingly. If you don’t need to own bonds at a derisory yield that fails to compensate you adequately for inflation or currency or credit risk, hold something else instead.

A brief post-script. Some years ago we went to see an exhibition of watercolours by Francis Towne at the British Museum. Although Towne’s genius went unrecognised in his lifetime (1740 – 1816), he is now acknowledged as one of the finest painters of his day. At the peak of his career he would create a series of watercolours of Rome and its ruins. (See this commentary for more on the theme of ‘Ozymandias’ and the hubristic decline of a once dominant civilisation).

The notes accompanying the Towne exhibition had an ominous relevance to the UK and to the possible fate of the European Union – a now badly wounded political union and ailing economic union facing multiple existential crises that had its origins in the international agreement known, of course, as the Treaty of Rome:

“During Towne’s lifetime, Imperial Rome was an inspiration and example for artists and thinkers in Britain. In 1776 Edward Gibbon first published his monumental History of the Decline and Fall of the Roman Empire. Gibbon argued that the ancient civilisation had collapsed after its civic-minded lifestyle gave way to luxury and factionalism.

“Britain had itself recently suffered a series of crises, including the revolt of the American colonies and the prosecution of parliamentary reformer John Wilkes. Towne, and his circle of friends based in Exeter, drew parallels between the political situation of Britain and that of ancient Rome. They believed the country was being misruled by a London-based metropolitan elite, and that Britain needed to return to the frugal and uncorrupted values of the provinces.”

Nothing to add.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio – with no obligation at all:

…………

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com.

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks and real assets, and also in systematic trend-following funds.

Brilliant use of the Vesuvius analogy! The parallel between ancient Romans not having a word for volcano and modern investors not recognizing the bond market danger is well-drawn. I had a similar realization back in 2020 when I started repositioning out of fixed income, the shift from that 40-year downtrend really does feel like one of those slow-motion earthquakes nobody wants to acknowledge until its too late.

Excellent analogies here and warnings about what risk actually means. I wonder, though, can gold serve the role of base collateral in the world today? after all, since the amount is not going to increase very quickly, the price will need to do a lot of work to underpin the nominal value of outstanding debt and transactions. consider there are over $300 trillion in debt outstanding around the world. does that mean gold needs to go to $50k, or are we looking at a major deflation/depression as debt is repudiated?