“If you think deflation is a fact of life, you clearly haven’t paid attention to history.”

—

—

“I think it is obvious that we’ve finally reached the limits of monetary policy. Does the ECB taking rates 10 basis points more negative do anything but accelerate the bankruptcy of the Eurozone banking system? Does it increase consumption or capital expenditures? Of course not. If anything, it just starves the system of capital by taking everyone’s return on capital investment down towards zero and below. Who invests when expected returns are negative? What the world needs is a big reset of the system where leveraged firms default, solvent firms pick up the pieces and get to earn excess returns due to their past fiscal sobriety. Since we live in a democracy, that won’t happen, instead we will have extreme fiscal stimulus in order to kick the can further down the road..

“In October, I spent 15 hours in the Sheremetyevo airport in Moscow (damn connecting flight never showed). It hasn’t seen a dollar of cap-ex in years, but it’s still light years ahead of LaGuardia or LAX. Just wait until corporations learn how much they can make from a never-ending airport renovation project. Now multiply that by hundreds of airports in America that desperately need capital investment. Now add bridges, roads, bullet trains, water infrastructure and our electrical grid. Why are all the lobbyists trying to get us into wars with third world nations? Corporations would make more money fixing our infrastructure and it’s going to be a lot less politically contentious.

“If you think deflation is a fact of life, you clearly haven’t paid attention to history. Governments around the world have experienced a unique decade where they ran deficits and printed money without “bad inflation” which upsets voters. They think this is a new normal with no consequences. It isn’t. They’re already panicking with the S&P a few ticks from all-time highs. Soon politicians will go into ludicrous mode with fiscal stimulus.

“What will fiscal stimulus do to the equity market? I’m reminded of the 1970s—inflation is no friend to most stocks. What happens to trillions in negative yielding long-dated bonds if inflation ticks up? What happens to bond proxies like global large-cap equity indexes or real estate? What happens to risk-parity funds that are leveraged a few times over expecting bonds and equities to increase over time? What if both legs of the trade drop at the same time? No one is ready for inflation, but I believe it’s coming. Maybe not today or next week, but there is a powder keg of monetary supply just waiting to be unleashed by governments who think that inflation can never happen again. At first, markets will cheer a bit of inflation—then they’ll panic. The markets often do whatever the fewest people are positioned for. Who’s positioned for inflation? That’s about as contrarian as buying Argentine sovereign debt.

“I think the road-map ahead is a market crash, followed by obscene fiscal stimulus. As always, I’m trying to think a few steps ahead here. I’m making a list of beat-down sectors who benefit from this change in government policy. I want to be ready to buy as soon as they get serious about unleashing the stimulus. You need a crisis that’s severe enough that both political parties can agree on stimulus. We’re not there yet, but we will be. If you thought QE was nutty, wait until you see what drunken sailor mode looks like. Inflation is coming. Be VERY careful if you own assets with duration risk.”

Harris Kupperman, ‘Inflation is Coming’, 4 December 2019.

This commentary was first published in January 2020 – yes, from another age. We republish it here and now because it feels at least as relevant today.

The commentary will now be taking a short break.

As Ian Fleming put it, once is happenstance. Twice is coincidence. Three times is enemy action. Well, not to put too fine a point on it, ‘Inflation is Coming’ was the first, recent, entirely credible inflation jeremiad we stumbled upon. ‘Debt, Austrians and Investment Strategy’ was the second – by Sir Steven Wilkinson (incidentally one of the best guests we’ve ever had on the State of the Markets podcast). Sir Steven’s original piece is worth the reading, but here’s a taster:

“..I am currently unsure of whether I have manoeuvred myself into an echo chamber of a clique of like-minded value investors who can see clearly that we are in “Fergie time” and thus close to a cataclysmic popping of the Everything Bubble (including money) or whether the current narrative (dangerously close to the end of the Everything Bubble, so man the life-boats) is now the popular view and therefore discounted? My view is coloured strongly by a moral conviction that what we have now (broken money, punishment of savers, risk free reward for insiders, etc.) is simply wrong and possibly even evil at a societal level, so what I think will happen and what I believe should happen (to purge the system of moral turpitude) are conflated at the margin. The technocratic disregard of the concerns and values of the saving classes personified in the ghastly Ms. Lagarde‘s most recent comments disgust me personally.

“The question, as always, is what to do in times of great uncertainty and possibly at bifurcation points of historical dimensions, a point I have made elsewhere with reference to the need – borrowing from Howard Marks of Oaktree Capital – to “move forward, but with caution”..

And Henry Maxey’s ‘Dismantling the Deflation Machine’ is now the third (hat-tip, en passant, to Duncan MacInnes). Mr. Maxey’s piece will feature in the Ruffer Review 2020, but here is the synopsis:

“Seeking to escape the inflation of the 1970s, policymakers have inadvertently engineered an equally powerful deflation machine. Over the past 30 years, this has been mightily reinforced by the transformation of China’s economy and the impact of technology.

“Today, a financial system that is structurally intolerant of inflation faces a changing political-economy regime that makes inflation inevitable. The markets have wired themselves to the wrong inevitabilities.”

“Asset and wealth managers – and their clients – need to be prepared for some of the most important changes for a generation.”

We agree.

There are a few problems here. One of them is that some of us have been expecting a rather messy outbreak of inflation since the first desperate Basil Fawltyish QE experiments began roughly a decade ago. Turns out we were simply looking in the wrong place (there’s been no shortage of inflation in the prices of financial assets – someone should perhaps have told the likes of Mark Carney or Mario Draghi). Another problem is the perennial boy-crying-wolf scenario. We console ourselves there with the linguistic solace of Grant Williams in that “hasn’t” is not the same as “won’t”. Yet another problem is that a generation of investors don’t remember the 1970s. These people are dangerous enough to vote for Jeremy Corbyn. Little do they appreciate that any remote kind of rerun of the 1970s will be more dangerous for their wealth even than Jeremy Corbyn.

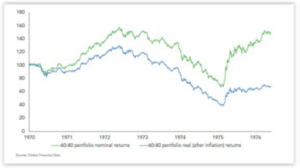

There will be little comfort to come from conventional asset diversity in the event of a rather messy outbreak of inflation. As Henry Maxey points out, the traditional 60/40 Equity / Bond portfolio did not exactly pass the 1970s stagflation test with flying colours.

Performance of a 60/40 Equity / Bond portfolio during the 1970s

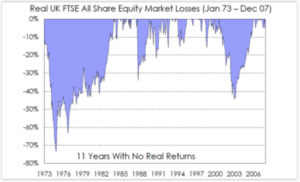

Then look at the two main asset classes in isolation. The following charts are courtesy of Frontier Capital Management. First, how did stocks fare ?

Answer: not that well. In real terms, equity investors during the stagflationary 1970s endured a drawdown of over 70%. Worse yet, they had to wait 11 years to get their money back.

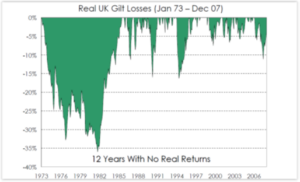

Then there were bonds.. How did they fare ?

Not exactly peachy. The drawdown for Gilt investors was “only” 35% – but they still had to wait 12 years to get their money back.

Given that stock market multiples are far higher today and bond yields are already dismally lower, it is difficult to envisage today’s 60/40 portfolio blithely sailing through the squalls of a rather messy outbreak of inflation.

By way of investment policy, here is our approach:

1) Concentrate equity exposure on only the most seemingly bulletproof businesses with principled, shareholder-friendly management, and only then when the shares of those businesses can be purchased at no obvious premium to their underlying inherent value, and ideally at a discount instead.

2) Avoid bonds altogether. Invest apophatically though, and don’t try to be smart by speculating in hugely time-sensitive shorting of markets that long ago stopped obeying reason, logic or economic reality.

3) Own portfolio insurance offering the uncorrelated potential for strong absolute returns (in our world, this means owning some of the best systematic trend-following funds).

4) Own real assets offering some degree of inflation protection or at least damage limitation.

On this last point, two further questions naturally arise. 1) Got gold ? 2) If you do “got gold”, do you really have enough ?

Of course, we may not get that (long anticipated) rather messy outbreak of inflation. How confident are you of that ? Mesdames et messieurs, les jeux sont faits.

………….

As you may know, we also manage bespoke investment portfolios for private clients internationally. We would be delighted to help you, too. Because of the current heightened market volatility we are offering a completely free financial review, with no strings attached, to see if our value-oriented approach might benefit your portfolio -with no obligation at all:

Tim Price is co-manager of the VT Price Value Portfolio and author of ‘Investing through the Looking Glass: a rational guide to irrational financial markets’. You can access a full archive of these weekly investment commentaries here. You can listen to our regular ‘State of the Markets’ podcasts, with Paul Rodriguez of ThinkTrading.com, here. Email us: info@pricevaluepartners.com

Price Value Partners manage investment portfolios for private clients. We also manage the VT Price Value Portfolio, an unconstrained global fund investing in Benjamin Graham-style value stocks.

Tim - this is terrific stuff and how prescient was Harris Kuperman? I suppose it is just a matter of looking at things realistically.

It struck me that it would be very valuable for you to put on a paid Webinar with a title like - Investing and Asset Protection in a Time of Uncertainty or something like that. The problem with most of we non-clever investors and normies is that we don't know what we don't know. Having an overview from you and the key strategies plus a Q&A session would be something that many would be pleased to pay for.